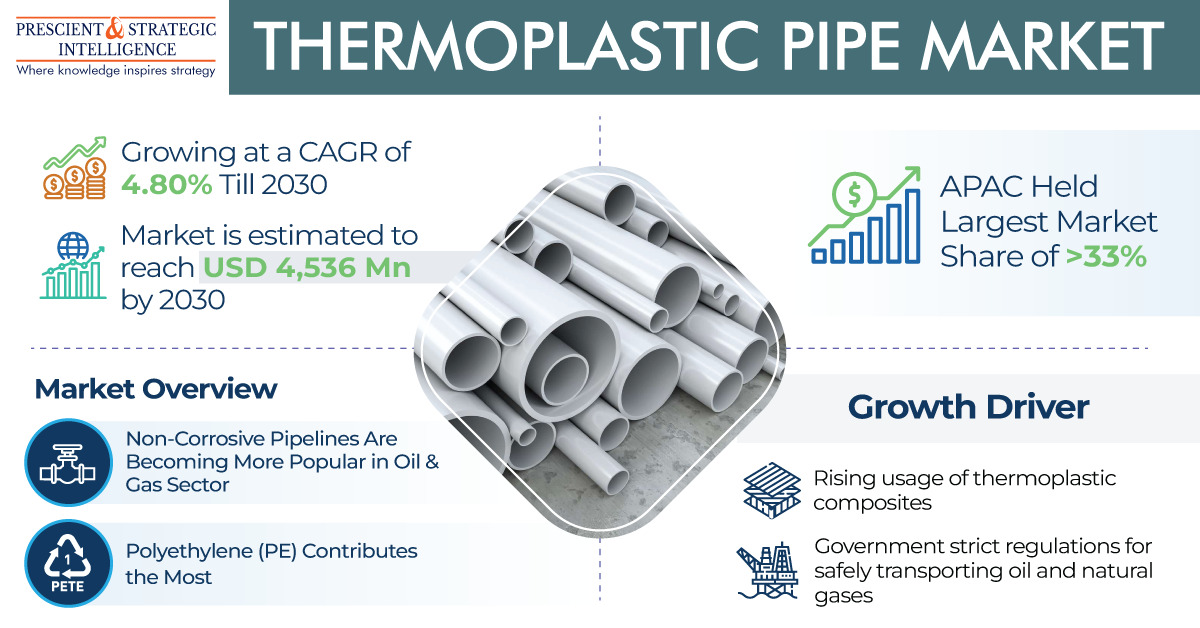

The thermoplastic pipe market was USD 3,117 million in 2022, and it will propel at a 4.80% compound annual growth rate, to touch USD 4,536 million, by 2030.

The growth of the industry is because of the surging acceptance of renewable energy, the mounting adoption of engineering thermoplastic materials, the increasing applications of large-diameter pipe, and the expanding oil & gas industry.

In 2022, the reinforced thermoplastic pipe category, based on product type, dominated the industry, with over 60% share, and it will remain dominant in the years to come. This is attributed to the fact that reinforced thermoplastic pipe is primarily utilized for sewage treatment, high-pressure alcohol injection, hydrocarbon transportation and extraction, and oilfield water injection.

Whereas, the thermoplastic composite pipe category is expected to observe significant growth in the years to come. This is attributed to the fact that it is a substitute for steel, which is an important material in the oil & gas industry. Moreover, it is often utilized in offshore applications such as risers and pipelines for chemical injection.

In 2022, the polyethylene category, based on polymer type, accounted for the largest thermoplastic pipe market share, of approximately 32%, and it will remain the largest in the years to come. This is credited to the fact that it can be utilized in low temperatures without the risk of brittle failure.

For the applications of low-temperature heat transfer, such as radiating floor heating, snow melting, underground ground source heat pump pipes, and ice rinks, it generates a substantial use for specific PE piping formulations.

In 2022, the oil & gas category, based on end use industry, held the largest share, of approximately 43%, and it will also remain the largest in the years to come. This is because of the extensive application areas for such pipes, such as transportation pipelines, domestic, and flowlines; the growing requirement for corrosion-less pipes that need less maintenance; advancement in technology; and the growing number of gas transportation pipeline projects.

APAC dominated the industry in 2022, with an approximately 33% share, and it will remain dominant in the years to come. This is because of the increasing number of oil & gas practices, the rising number of local manufacturers, the growing capacity of oil & gas production, and the arrival of global players to set up their manufacturing facilities because of the easy accessibility of cheap labor and raw materials in the continent.